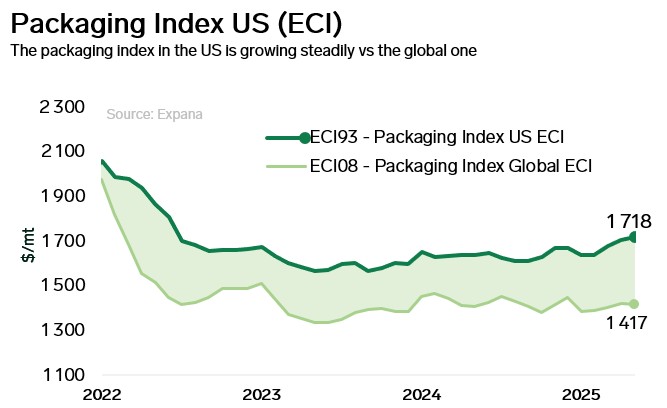

The Expana US Packaging Category Index (ECI) rose by 0.7% month-on-month (m-o-m) and 5% year-on-year (y-o-y) in August to $1,718/mt. A steady increase in the index has been observed since June, driven by tariff policy. The main growth driver is metal packaging, which was hit with 50% import tariffs. In August, warehouse prices for aluminum cans increased by 1.8% m-o-m and 10.3% y-o-y, foil rose by 1.6% m-o-m and 30.5% y-o-y, and tinplate on the spot market jumped 4.5% m-o-m and 18.2% y-o-y. Prices for packaging paper were relatively stable m-o-m, but still grew 2–10% y-o-y depending on the product.

Metal tariffs are driving up the US packaging index. Compared to the global packaging index, the difference increased to $300/mt in August from $252/mt in May. It is therefore clear that the introduction of tariffs creates rising packaging costs in the US.

Demand for packaging materials in the US remains stable, but cost pressure is intensifying against the backdrop of rising tariffs. In 2025, the main consumption drivers remain the food, pharmaceutical, and e-commerce sectors. Sales in these categories continue to expand; retail trade volumes rose 3.9% y-o-y in July, while the Food Production Index has been growing steadily since the start of 2025, adding about 0.2% quarter-on-quarter (q-o-q). This underpins sustained demand for primary and secondary packaging made of paper, board, and lightweight plastics.

On the cost side, producers are facing higher raw material costs, primarily due to stricter tariff policy. In the first half of 2025, aluminum and steel tariffs were raised to 50%, directly affecting can and foil packaging producers. Imports of aluminum scrap, which are not yet subject to tariffs, are containing further price growth. However, the gap between global and domestic prices is widening, reducing competitiveness.

In the paper market, the US still has excess capacity, which generates high supply, although about 6% of containerboard capacity has been removed since the start of 2025. These closures boosted both industrial production and capacity utilization as demand from shuttered mills shifted elsewhere. Consumer and retailer packaging preferences are shifting toward paper in the long term, thanks to recyclability and low-carbon manufacturing. EPR laws in some states are starting to provide financial incentives for using more recyclable materials, including paper.

Plastic producers are cutting production to match demand. In July, the US Manufacture of Plastics Products Index fell by 1.6% m-o-m, representing a 4.3% y-o-y decrease. Some disruptions were reported throughout the month, and sources remain cautious about hurricane impacts, with Hurricane Erin forming in August but causing no damage to plastics manufacturing. Export demand for plastics, however, is growing. Total exports of ethylene and propylene polymers increased in June by 7.7% m-o-m, representing a 7.2% y-o-y rise. Ethylene polymer exports rose by 9.0% m-o-m, while propylene polymer exports fell by 0.5% m-o-m.

Glass container manufacturing costs in the US fell by 0.6% m-o-m in August. The decrease was attributable to lower energy prices, particularly in the natural gas market, which had a bearish impact on overall glass manufacturing costs. Sales of alcoholic beverages rose slightly, according to the latest data from the Board of Governors of the Federal Reserve System. However, the long-term trend shows decline, with glass container manufacturing also falling, showing supply decreasing to balance sluggish demand.

Image source: Shutterstock

Written by Artem Segen