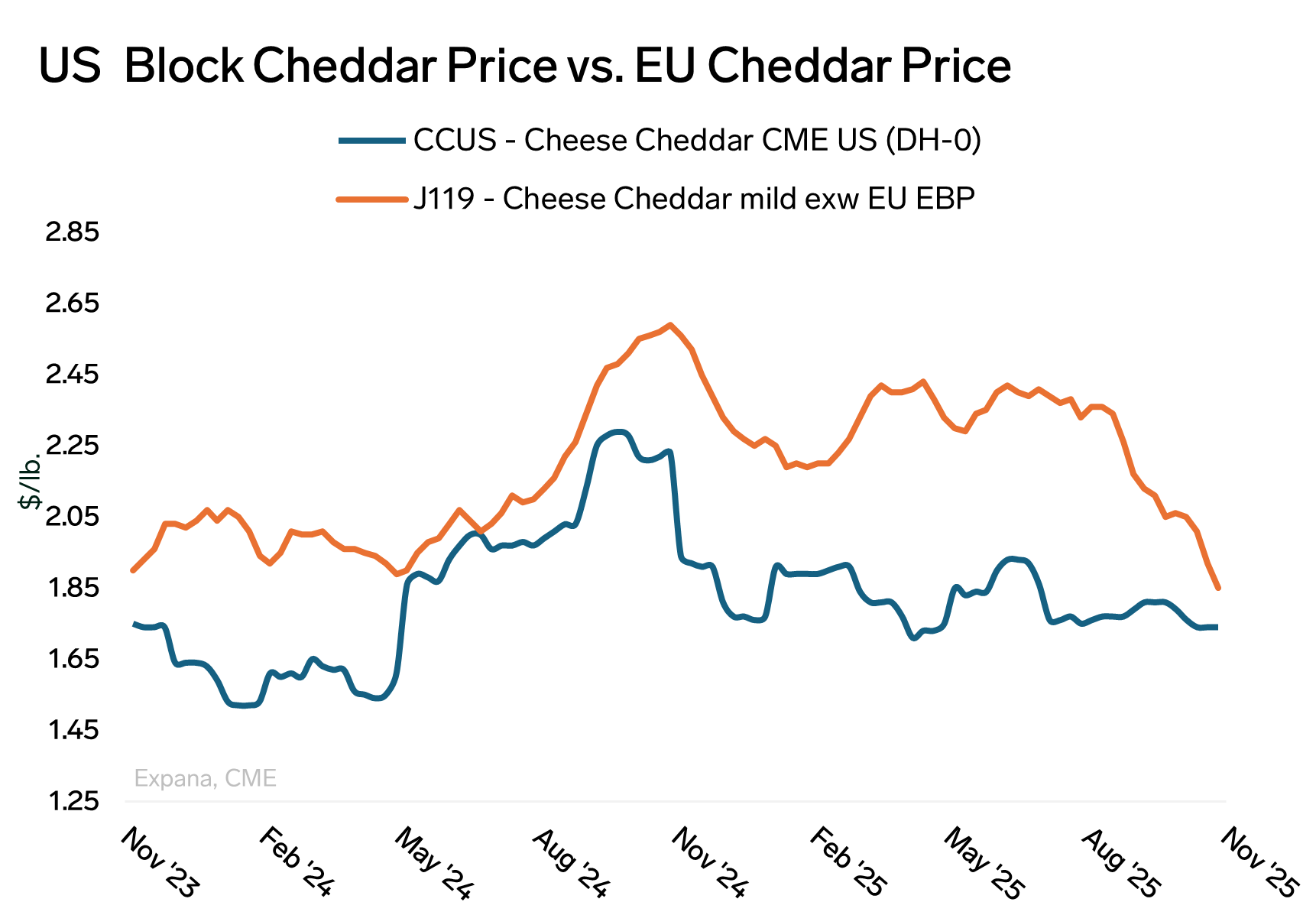

The price gap between US CME block cheddar prices and EU cheddar spot prices has narrowed to the smallest difference since summer 2024. For all of 2025, US cheddar traded at a persistent, sizable discount to European production, largely driven by ample milk supplies, steady to weak domestic demand, and growing production. Those fundamentals supported aggressive export competitiveness for most of the year, and US cheese shipments ran well ahead of year-ago volumes.

However, market dynamics began to shift during the month of October. Several major US cheese plants reported downtime, cutting output and prompting a rapid drawdown of inventories amid continued export activity. Market contacts report that spot cheddar has been tight for roughly a month, which has added upward pressure to domestic prices and narrowed the usual US price advantage.

In contrast, the European cheddar market has moved consistently in the opposite direction, with prices dropping by over 30% year-over-year. Unseasonably strong milk flows across key producing regions have sustained heavy cheese output while demand remained steady to weak, placing sustained downward pressure on prices and boosting the attractiveness of EU products on global markets, further intensifying pressure on US exporters.

US price competitiveness has eroded in recent weeks, and exports have softened as buyers increasingly favor EU and New Zealand offers due to increasing price advantages.

Image source: Getty

Written by Brittany Feyh