During Q1 2026, unusual weather conditions observed in Colombia initially looked to be impactful for coffee production in the country as recent production and export statistics reflected a downtrend. Yet, subsequent weather patterns may minimize any downward revisions in Colombian coffee production.

Previously, flooding and increased rainfall were believed to have curtailed coffee production across the country that is one of the top global producers of quality, green arabica beans in South America according to multiple sources noting the excessive rainfall which persisted until just recently.

However, generally high coffee prices have stimulated advanced farm care, according to Expana’s fundamentals team (formerly Tropical Research Services) who noted in the most recent crop survey that more favorable weather conditions are in the forecast.

What’s more, the rainfall may have only delayed coffee production and exports—rather than made significant impacts to total production and export numbers, according to Expana’s Senior Manager of Coffee Analysis, Oliver Broster.

“Rain came early, and everyone was worried,” said Broster. “But it dried out, and the pattern flipped. So, the net effect: It works out OK… The main crop should be good again. While it’s not ideal, it’s not bad either.”

Broster also recognized the recent phenomenon of slow coffee sales from certain producing regions.

“It’s not really weather related,” continued Broster. “More people are not selling coffee as quickly—they’re selling more slowly—not liking fact that prices are going lower.”

On April 24, contract values of arabica bucked the sideways trend—pulsing higher 4.61% from the previous day. While prices in each origin are subject to varying factors, nearby contract prices for arabica coffee on NY ICE most recently closed at 316.35 USc/Lb, according to the Expana platform which shows a rollercoaster of a year for the commodity’s value. Over the last five years, contract prices are up approximately 131%.

“Global export numbers are strong,” said Broster. “But not in Brazil, and Colombia is down too.”

While producers in certain regions have grown accustomed to the last five years of higher coffee prices (and thus have held their coffee hoping to see those prices again), other producers in places like Honduras instead took advantage of the current price levels when the harvest came in, said Broster.

“In Colombia, the coffee’s there, but it’s taking more time to come to market,” shared Broster. “But in Honduras, producers saw great price and sold. I think they’ve done the best out of everyone. But the crop will be frontloaded there, and Honduras will run out of coffee earlier than others. For example, exports are running ahead of where they were last year, and [where they] have been historically. It does appear that the crop will be front loaded, which makes sense given high price levels and the market structure.”

Colombia’s Coffee Conundrum

On April 10, lower production and export numbers out of Colombia caused some market panic.

“Between January and March, production reached 2.51 million 60-Kg bags, compared to 3.78 million in the same period of 2025, representing a drop of approximately 33.5%,” according to Germán Bahamón, the National Federation of Coffee Growers (Fedecafé) general manager.

Despite the released statistics, Expana’s fundamentals team is of the opinion that Colombia’s coffee numbers will even out as the year progresses.

Previously, flooding had been a problem across multiple areas in Colombia’s coffee growing regions, noted Market Reporter, Sammy Rolls.

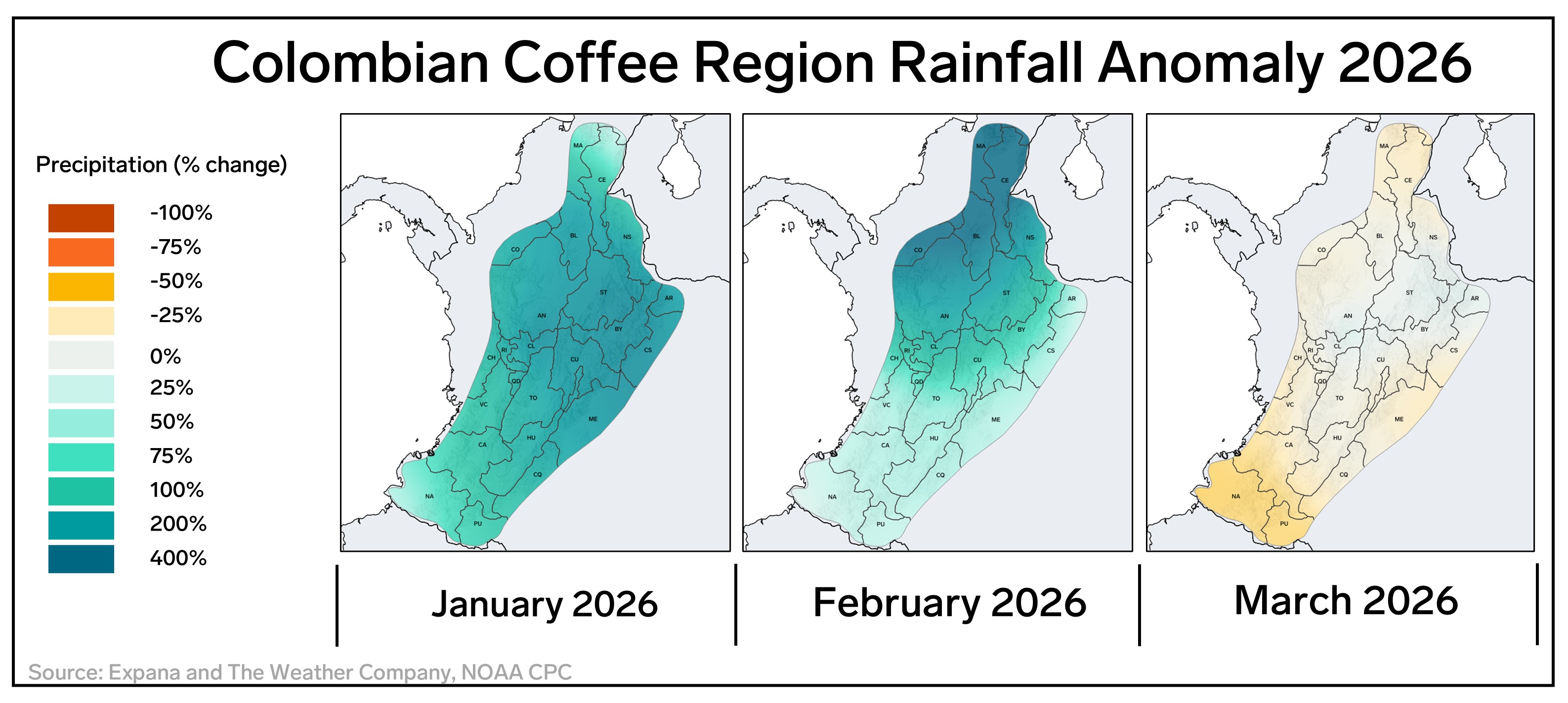

Rainfall percentage change from the 30-year average in Columbia’s primary coffee region, during January, February, and March 2026. Credit: Expana’s Weather & Crop Researcher, James Tyler.

Meteorological conditions during early February brought persistent, intense precipitation that triggered river overflow and widespread inundation, with some areas seeing rainfall exceeding 40-70 MM/day and flooding affecting large portions of northern Colombia between February 1-3. In Cordoba alone, flooding from late January onward impacted hundreds of thousands of residents, with emergency agencies reporting that over 80% of the department was affected and tens of thousands of families displaced as of mid-February to March 2026. The pattern of persistent rainfall continued into March, sustaining flood conditions and prolonging agricultural disruption across rural areas, according to Rolls who cited data from Expana’s weather team.

However, there is a discrepancy between rain and flooding in coffee areas versus other areas in the country, Broster reminded.

Colombia’s coffee sector saw a sharp setback in March, as persistent and heavy rainfall weighed on production in the world’s largest supplier of washed Arabica, according to Rolls. Output fell 29% year-over-year to 754,000 60-Kg bags, down from 1.06 million a year earlier, according to the Fedecafé statistics.

However, Expana’s numbers differ from those released by Fedecafé, according to Broster.

Each year, April produces the lowest amount of coffee as the new harvest begins this month. So, the months before April are often marked by generally higher production and exports.

“In foreign trade, the lower availability of coffee has a direct translation. Accumulated exports at the end of March reached 2.56 million bags, compared to 3.59 million in the same period of 2025, with a reduction of -29%,” wrote Bahamón.

The Expana Benchmark Price assessment of Colombian Arabica differentials reflects the tightening supply backdrop in the market. At the end of December 2025, the assessment stood at USc 22/Lb. But, as of April 20, 2026, it has since nearly doubled, reaching USc 40/Lb.

“The sharp rise aligns with deteriorating production conditions and weather-related disruptions in Colombia, which have reduced availability and supported stronger physical coffee differentials in early 2026,” according to Rolls.

“Neighboring coffee producers have shown a mixed but generally more resilient weather picture compared with Colombia. In Peru, production conditions have been relatively steadier, with rainfall patterns described as more seasonal and less disruptive in early 2026, supporting a broadly stable outlook for Arabica flows, although localized variability in the northern growing areas has still required monitoring. In Ecuador, conditions have been broadly neutral to slightly supportive, with no major widespread weather shocks reported and output expectations remaining comparatively steady versus Colombia’s weather-hit decline. In contrast, Brazil has seen generally favorable rainfall across key Arabica regions during late 2025 and early 2026, with improved soil moisture supporting crop development and underpinning expectations of a stronger harvest cycle, making conditions materially better than Colombia’s heavily rain-disrupted production environment this season,” according to Rolls.

Image source: Shutterstock

FAQs

What is happening to Colombian Arabica differentials?

Physical coffee differentials have tightened sharply. Expana’s Benchmark Price assessment for Colombian Arabica differentials nearly doubled between December 2025 and April 2026, moving from USc 22/lb to USc 40/lb — reflecting the reduced availability of Colombian beans in the market.

Why are Colombian producers holding back coffee from the market?

It is less about weather and more about price expectations. Producers who have grown accustomed to five years of elevated prices are reluctant to sell at current levels, hoping prices will recover. This is slowing the flow of coffee to market independently of any weather-related supply issues.

How have neighbouring countries been affected?

The picture is mixed but generally more resilient than Colombia. Brazil has seen favourable conditions and is expected to deliver a stronger harvest. Peru and Ecuador have both had broadly stable outlooks with no major disruptions. Colombia’s weather-driven decline stands out as the exception in the region rather than the rule.

Written by Ryan Gallagher