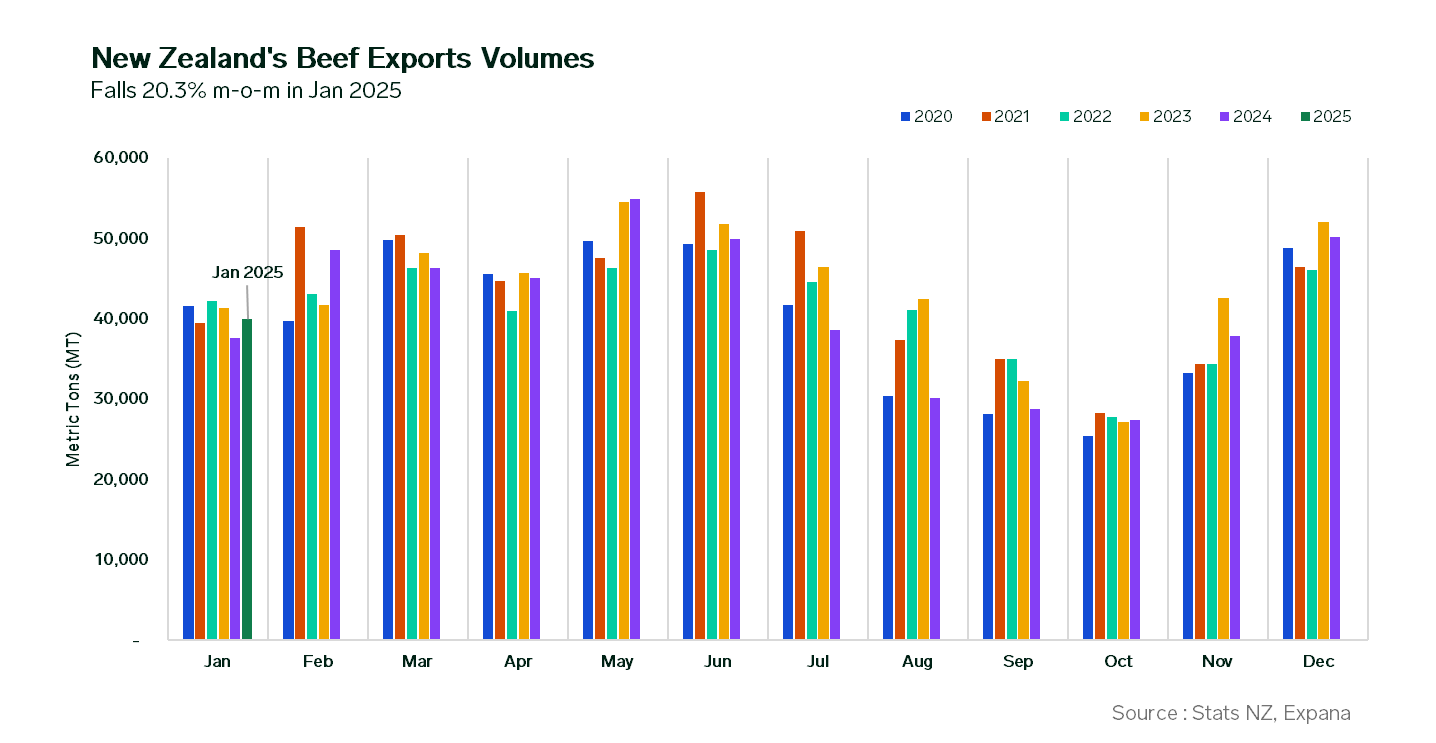

New Zealand’s January 2025 beef exports dropped 20.3% month-on-month (m-o-m) to 40,002 metric tons (mt), as shown in the latest Stats NZ data.

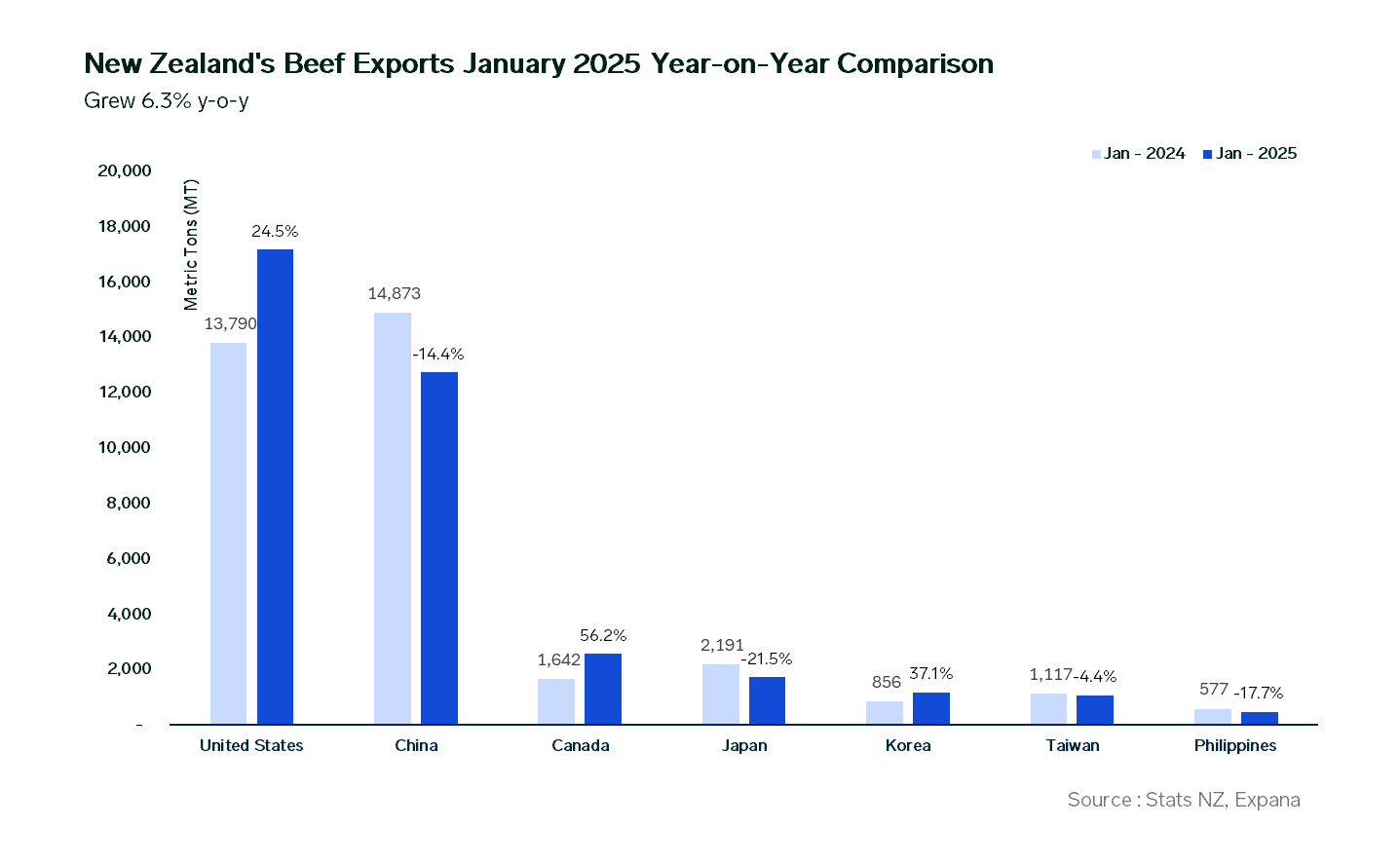

Falling by 10,161 mt, volumes were curtailed primarily due to the shorter working month as the country observed the Christmas and New Year festivities. Outbound shipments declined across all key markets. Annually, exports grew 6.3% (+2,369 mt), fueled by healthy demand from the US and Canada. However, shipments to China, once its largest trading partner, were limited by its economic struggles.

For all of 2024, New Zealand’s total beef exports were 5.6% lower y-o-y at 497,014 mt as the country continued to focus on herd retention.

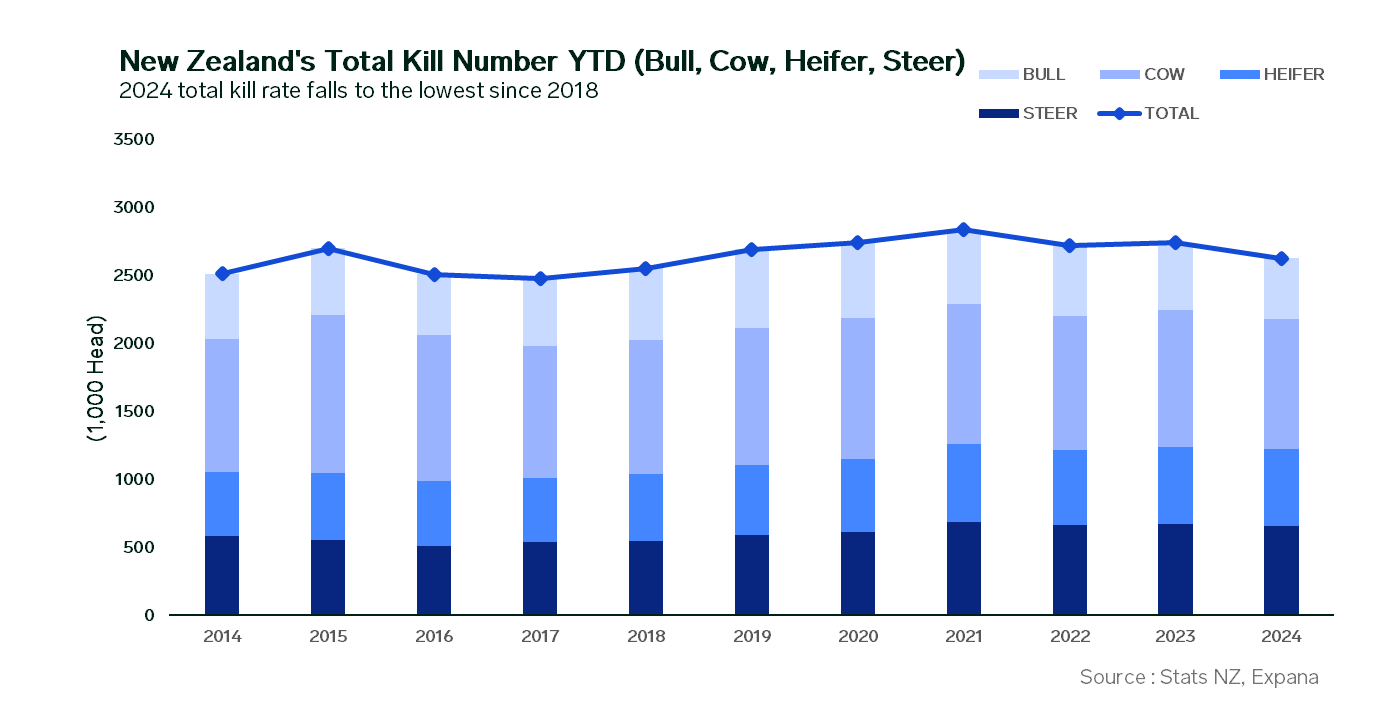

Official Stats NZ figures indicated New Zealand’s total livestock slaughter in 2024, covering bulls, cows, heifers, and steers, dropped to the lowest level since 2018, reaching 2.63 million head.

With an annual decline of 113,823 head, kill rates slumped 4.2% year-on-year (y-o-y), driven primarily by drought-induced destocking, particularly in the South Island. A reduction in breeding cows, along with fewer calves raised since 2022 due to profitability challenges, further tightened supply.

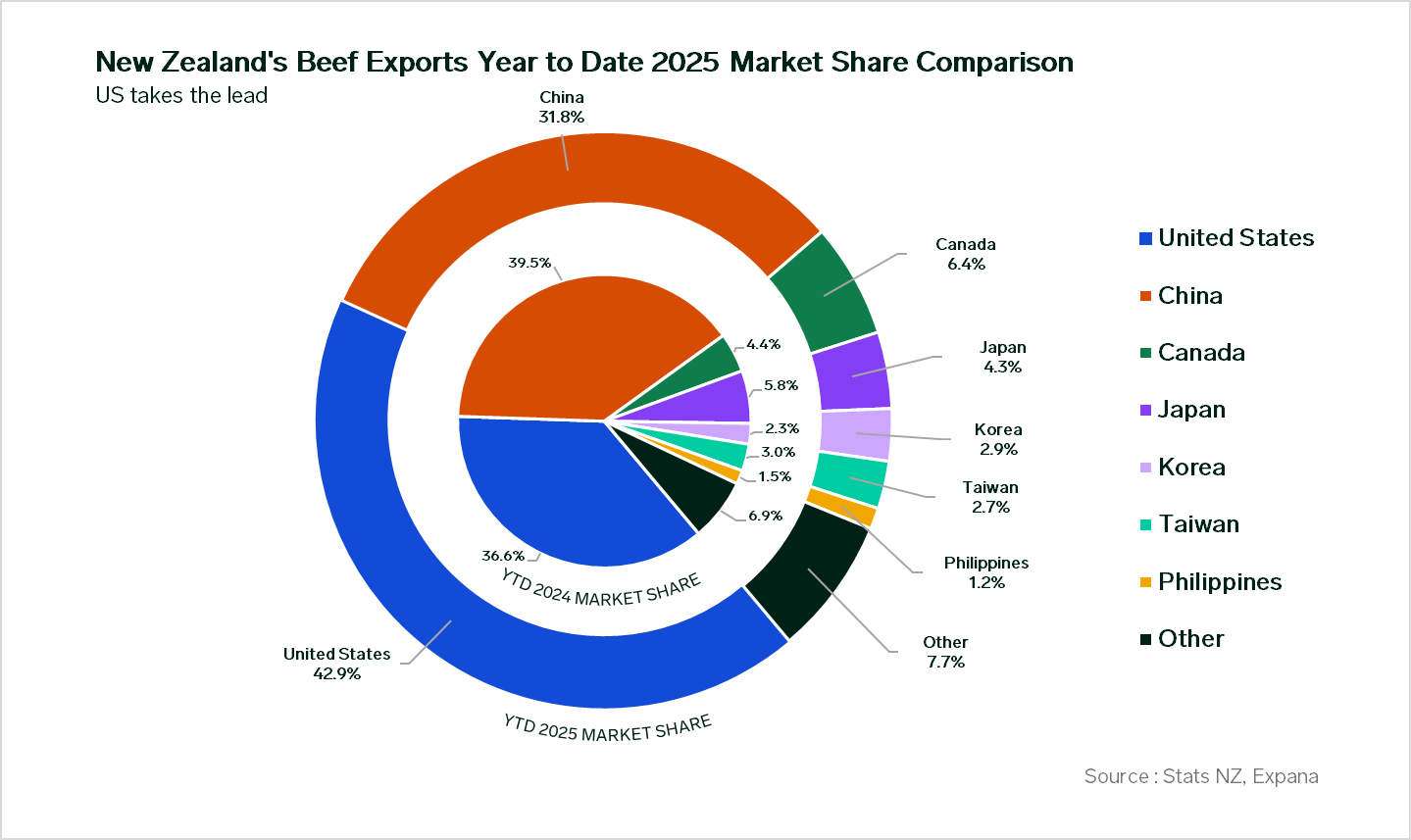

The United States

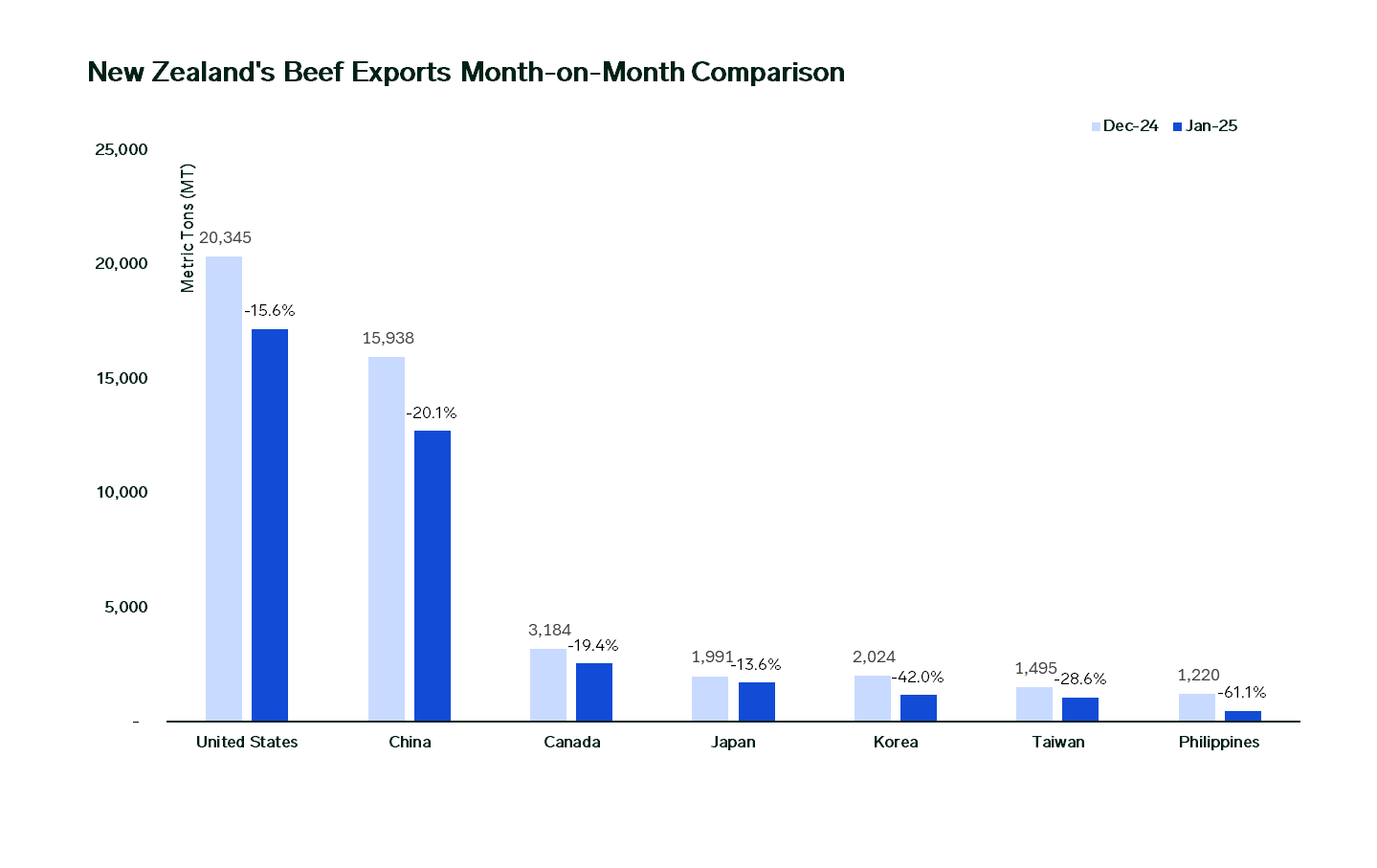

The US took the top spot as New Zealand’s largest destination in January 2025, with a market share of 42.9%. Exports dropped 15.6% m-o-m (-3,172 mt) to 17,173 mt as holiday closures during New Year celebrations temporarily halted operations.

Demand for pasture-raised lean boneless beef, a key ingredient in hamburgers and sausages, remained robust. On a yearly basis, exports grew 24.5% y-o-y (+3,383 mt).

Export pace to the US remained firm. By February 17, The Commodity Status Report from the US Customs and Border Protection indicated New Zealand utilized 11.65% of its export quota to the US for the 2024 calendar year.

The country is permitted to export 213,402 mt of beef and veal to the US annually, with the majority bound to an in-quota tariff rate of USD 4.4 c/kg. The out-of-quota tariff rate stands at 26.4%.

China

Fierce competition, driven by Australia’s high production levels and an influx of South American beef, led to a 27.8% drop in volumes destined for the Chinese market, falling by 20.1% (-3,206 mt) to 12,732 mt.

Despite this decline, China held on to its position as the world’s second-largest beef importer, with a 31.8% market share in January 2025. Annually, volumes tumbled 14.4% y-o-y (-2,141 mt), impacted by economic constraints in this price-sensitive market.

Canada

Holding third place, exports to Canada amounted to 2,565 mt, capturing a 6.4% market share. Volumes declined 19.4% m-o-m (-619 mt), primarily due to the holiday season.

Netbacks to Canada were sometimes more favorable than those to the US, particularly for lean boneless beef trimmings. This prompted New Zealand packers to prioritize Canada as a key market, with shipments rising a staggering 56.2% y-o-y (+923 mt) in January 2025.

Japan

Japan ranked as New Zealand’s fourth largest export destination, holding a market share of 4.3%. Total shipments to Japan in January 2025 reached 1,720 mt, slumping 13.6% m-o-m (-271 mt) compared to the previous month.

Despite Japan sourcing more beef from both Australia and New Zealand to fill gaps left by tightening US supply, shipments dropped 21.5% y-o-y (-471 mt) as high inflationary pressures kept demand subdued.

Korea

In the first month of the year, exports to Korea ranked fifth, reaching 1,174 mt and capturing a 2.9% market share. Volumes fell 42.0% m-o-m (-850 mt) as the country relied more on lower-tariff material from Australia and New Zealand. The Seollal holidays in early February also impacted shipments.

Despite Korea’s weak economic conditions, annual growth reached a stellar 37.1% y-o-y (+318 mt). This increase was driven by a reduction in US supply, which gave New Zealand the opportunity to capture more market share in this predominantly grain-fed market.

In 2025, beef exports to Korea are subject to a Free Trade Agreement (FTA) rate of 10.7%, down 2.6 percentage points from 2024’s 13.3%. In-quota volumes are set at up to 45,103 mt before the 24% Most Favoured Nation (MFN) tariff takes effect.

Tariffs to Korea are set to reduce to zero by 2030 under the Korea-New Zealand Free Trade Agreement (KNZFTA).

Other secondary export destinations in January 2025 include Taiwan (1,068 mt), the Philippines (475 mt), United Kingdom (463 mt), and Thailand (207 mt).

Expana provides regular beef market coverage for the geographies listed in this analysis. Click the link below to dive deeper in the beef market prices for different origins and destinations:

Co-authored by:

Joe Muldowney

1-732-240-5330 ext. 244

[email protected]

Bill Smith

Expana

1-732-240-5330 ext. 265

[email protected]

Written by Junie Lin