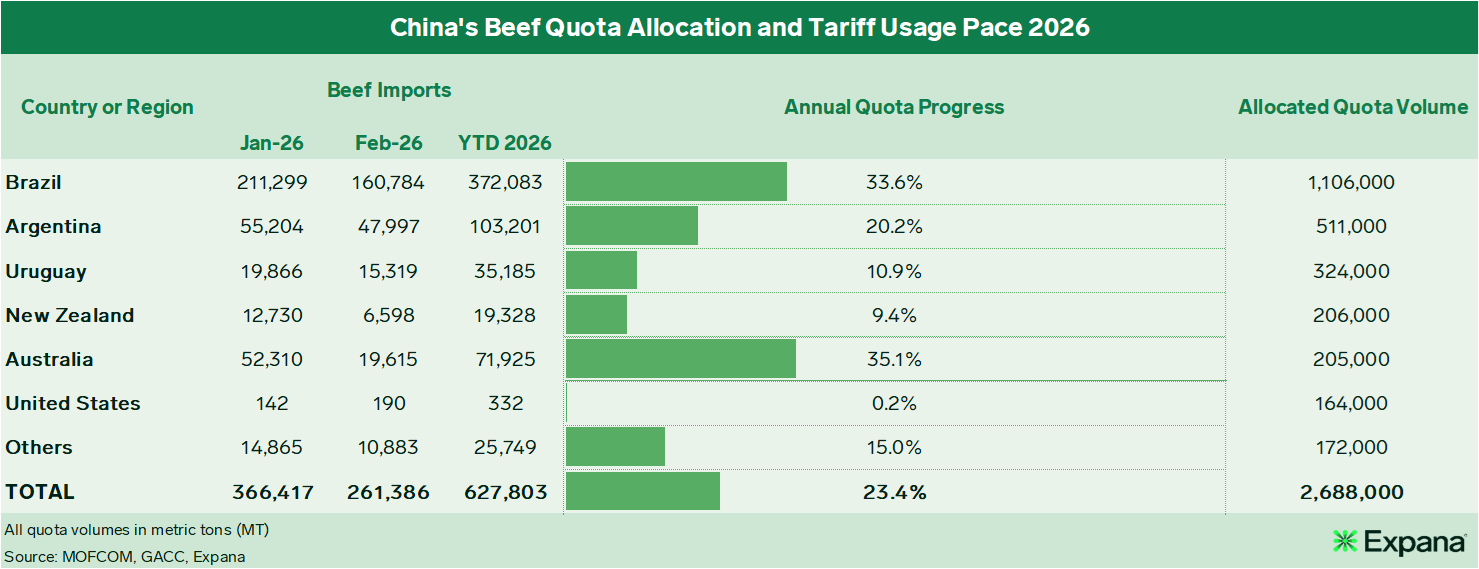

China’s total beef imports in January and February 2026 reached 627,803 metric tons (MT), representing a 23.4% utilization of the total annual safeguard quota, according to the latest data from the General Administration of Customs (GACC).

The current year-to-date (YTD) figures show a robust 34.0% volume increase year-on-year (YOY) as key suppliers raced to beat the newly implemented tariff “cliffs.”

China’s Safeguard Quota Crunch

China’s figures for the first two months of the calendar year were released together, as is customary to account for Lunar New Year distortions.

However, the underlying trend is clear: Beijing’s new safeguard policy, which kicked in on New Year’s Day, has triggered a “front-loading” frenzy among major suppliers.

Under this policy, any country exceeding its specific annual quota will be hit with a prohibitive 55% tariff for the remainder of the year.

China’s Domestic Glut & the Spending Squeeze

This fast start follows a cooling period in 2025, where beef imports totaled 2.80 million MT, a 2.5% yearly decline. This contraction was driven by a record liquidation of China’s domestic cattle herd, which flooded the market with local beef.

This shift is underpinned by an ongoing ‘consumption downgrade’, a trend gaining momentum since the pandemic as the property-market crisis and rising economic uncertainty continue to hollow out middle-class spending power.

This shift was accelerated by the official ban on alcohol introduced back in mid-May 2025. The policy has since created a chilling effect across the corporate and government sectors, continuing to impede spending on high-end beef in fine dining and banquets, segments that historically underpin demand for premium imported cuts.

(i) Brazil: The Heavyweight Sprint

Brazil remains the primary market focus due to its sheer scale.

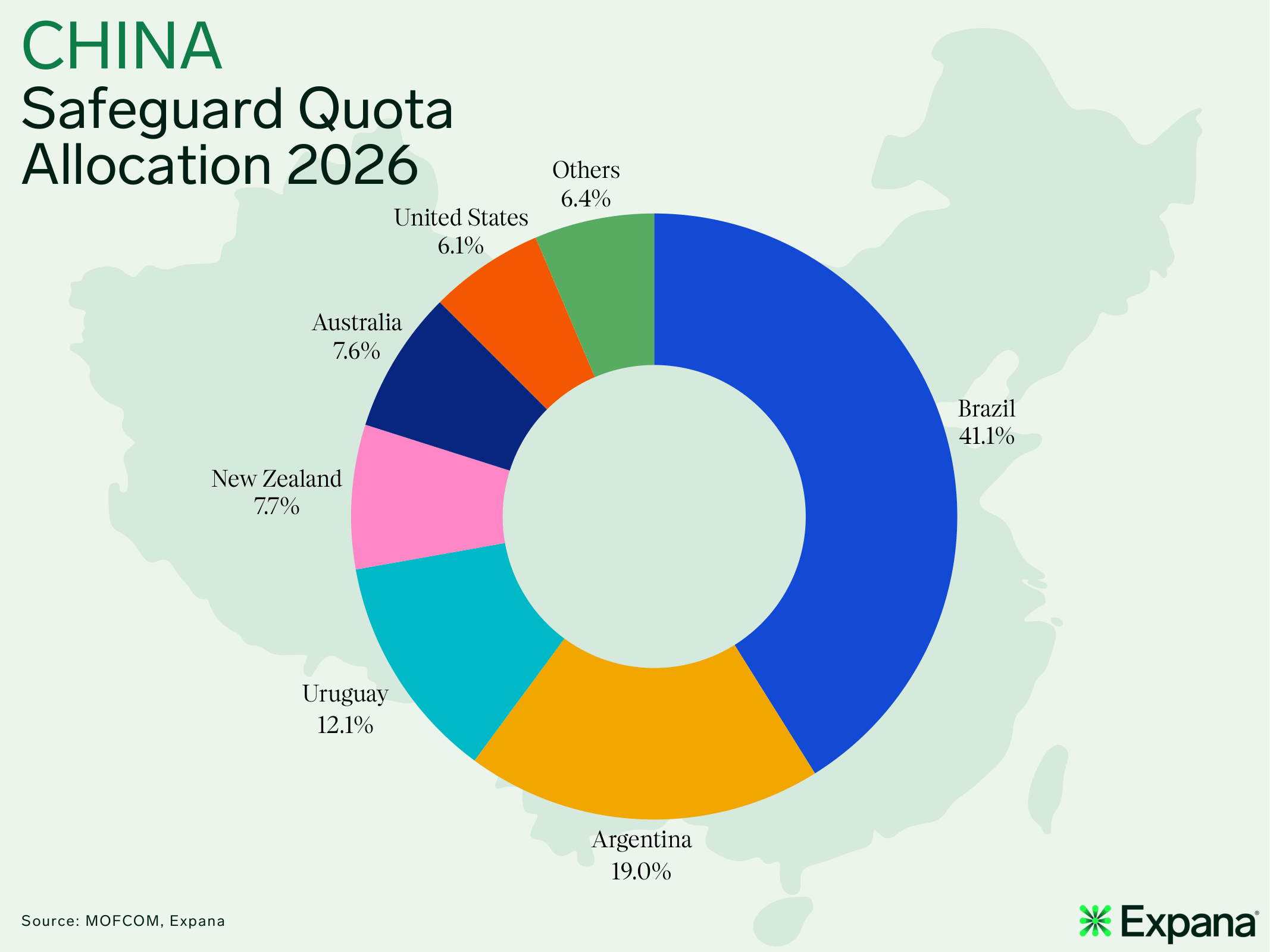

Despite holding the largest quota allocation of 1,106,000 MT, YTD volumes have already reached 372,083 MT, or 33.6% filled.

Volumes from Brazil saw a whopping 75.8% YOY surge, underpinned by a record-high in January 2026 taking into account cargoes previously held back in late 2025 due to stricter inspections which delayed clearance.

Having utilized roughly one third of its annual quota in just two months, shipments for the same period already totaled 223,426 MT, which is notably above previous year.

“Market participants estimated that Brazil could be on track to reach the quota limit by early Q3”, South American Red Meat Analyst, Augusto Eto said.

(ii) Australia: The Fastest Usage Pace

Australia currently faces the most immediate risk of exhaustion, burning through its allowance at the fastest pace of any major supplier.

With a YTD volume of 71,925 MT, it has already consumed 35.1% of its 205,000 MT allocation.

“At this pace, market expectations now suggest that Australia is likely to reach its ‘tariff wall’ by late May or early June, well ahead of its competitors,” Asia Pacific Red Meat Analyst, Junie Lin said.

“This compressed timeline effectively forces a strategic pivot; as the door slams shut on Australian volumes, New Zealand stands alone as the only neighboring alternative capable of providing a duty-free, risk-free pipeline for the remainder of the year.”, she added.

Inbound tonnage from Australia has seen a 27.6% YTD increase, similarly reaching a record-high volume in January 2026 as China cleared a backlog of shipments that had faced enhanced customs checks.

(iii) Argentina and Uruguay: Lower Risk Profiles

In contrast, volumes from Argentina and Uruguay pose a much lower risk factor due to slower utilization and larger relative buffers.

Argentina has used 20.2% of its quota, maintaining a steady flow of 103,201 MT YTD.

Uruguay remains the least exposed major South American player, having utilized only 10.9% (35,185 MT) of its 324,000 MT allocation, leaving ample room for year-end surges.

(iv) New Zealand: The Safe-Haven Option

With only 9.4% of its quota used YTD (19,328 MT), NZ exporters face virtually zero risk of triggering the safeguard tariff in 2026.

This frames New Zealand as the only ‘guaranteed’ duty-free source for the second half of the year once Australia hits its limits.

However, the real bottleneck for New Zealand is a lack of tangible product to export, as cattle kills are currently trailing almost 13% behind last year.

Furthermore, the lure of better margins in the United States (US) is actively diverting available supply away from the Chinese market.

(v) The United States: A Pipeline in Limbo

For the US, 2026 is proving that policy wins don’t always translate to trade volumes.

Following a 2025 where shipments nearly careened to a halt due to a “tariff blitz” and expired import permits, the market remains stifled.

While the Kuala Lumpur Agreement in November 2025 saw China agree to remove retaliatory tariffs, the recovery has been non-existent in the data.

YTD 2026 shipments sit at a negligible 332 MT (0.2% quota usage).

Yet, now in 2026, only still-eligible pipeline products are allowed entry, as the majority of US plants are still awaiting the renewal of lapsed CIFER registrations.

*Please note that import figures may vary from export data published by other official sources due to differences in the methodologies used by each entity/organization for collecting and reporting data.

Image source: Adobe

Written by Junie Lin, Augusto Eto and Bill Smith