Global steel production in the first quarter of 2026 continued its downward trend, but the structure of the decline proved more revealing than the contraction itself. In March 2026, steel output according to World Steel Association (WSA) fell 4.2% year over year (YOY), with the decline concentrated in Asia and particularly in the Middle East, while the US demonstrated growth. Overall, for the first two months of 2026, global steel production fell 2.3% YOY.

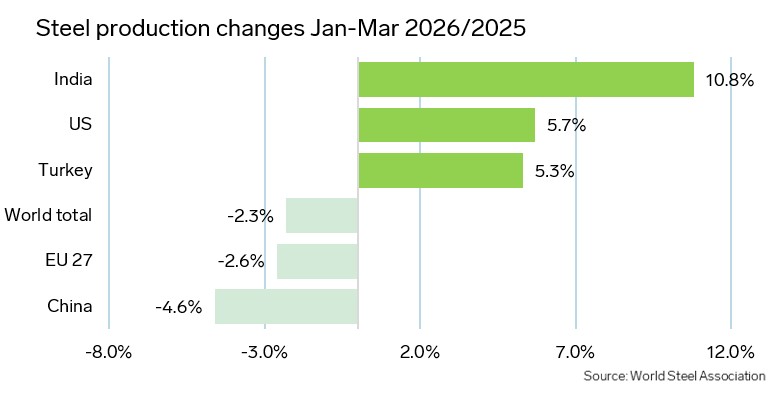

China remains the key driver of the decline, where production has fallen YOY for 11 consecutive months. Based on Q1 2026 results, China produced 54% of global steel and reduced output 4.6% YOY, reflecting weakness in the construction sector and restrictive policies toward excess capacity.

Despite demand recovery for steel produced within the EU, production in March still declined 4.6% YOY, confirming persistent pressure from limited end-user demand. Among the largest steel-producing countries, Germany is recovering production. At the same time, sources indicate that the Carbon Border Adjustment Mechanism (CBAM) significantly reduced imports, down 18% YOY in January 2026, so domestic steel production is expected to recover not only in Germany.

The US continues to grow steadily against the backdrop of import tariffs and recovery in domestic steel demand. Steel output in the US in the first quarter of 2026 increased 5.7% YOY. This widens the gap between the US and the rest of the world, where production overall is declining.

The most dramatic change occurred in the Middle East. In March, production fell 33.5% YOY, which sharply contrasts with growth in January and stability in February. This dynamic directly points to the impact of military conflict, which disrupted both domestic consumption and production chains in the region.

This production trend directly intersects with demand forecasts. WSA in its updated forecast from April 2026 expects global demand in 2026 to grow just 0.3%, substantially lower than previous expectations, with Middle East weakness and continued decline in China named as key negative factors. At the same time, demand growth outside China persists, and developed economies demonstrate moderate recovery, which aligns with production growth in the US and partial stabilization in Europe.

Thus, the market enters a fragmentation phase. China continues to drag down global metrics, Europe remains weak, the US is forming a local growth point, and geopolitics heightens volatility through sharp production and demand declines in the Middle East, which overall keeps the market under pressure and prevents transition to full recovery.

Image source: Getty

Written by Artem Segen