Key Takeaways

-

Chile supplies more than 70% of US fresh salmon fillet imports year to date through April

-

Norwegian fresh fillet shipments to the US are down 35% year to date as tariff pressure reshapes the import market

-

Frozen Atlantic fillet imports are tracking below the three-year average through the first four months of 2026

Chile controls more than 70% of US fresh salmon fillet imports, the Norwegian supply is down more than a third year-over-year, and a 12.5% tariff deadline is six weeks out. Despite all of that, the fresh benchmark is drifting lower, and buyers are hesitant to commit. The frozen market, running below a three-year average in volume, is the steadier of the two. Understanding why requires looking past the price series and into how Chilean producers get paid

The Structural Bias Toward Fresh Salmon

Chilean salmon producers have a built-in reason to favor the fresh channel: payment terms. Fresh fillet transactions typically settle within 30 days. Frozen sales routinely run 90 days or longer. That three-month difference in cash realization matters for a capital-intensive aquaculture operation managing feed costs and currency exposure. The result is that Chilean sellers keep fresh product moving even when prices soften, rather than absorbing the working-capital cost of putting it in the freezer. The trade data confirms it: Chilean fresh fillet shipments to the US are up 6.0% year-to-date through April 2026, while Chilean frozen shipments over the same period are down 2.2%.

What the Price Series Are Saying

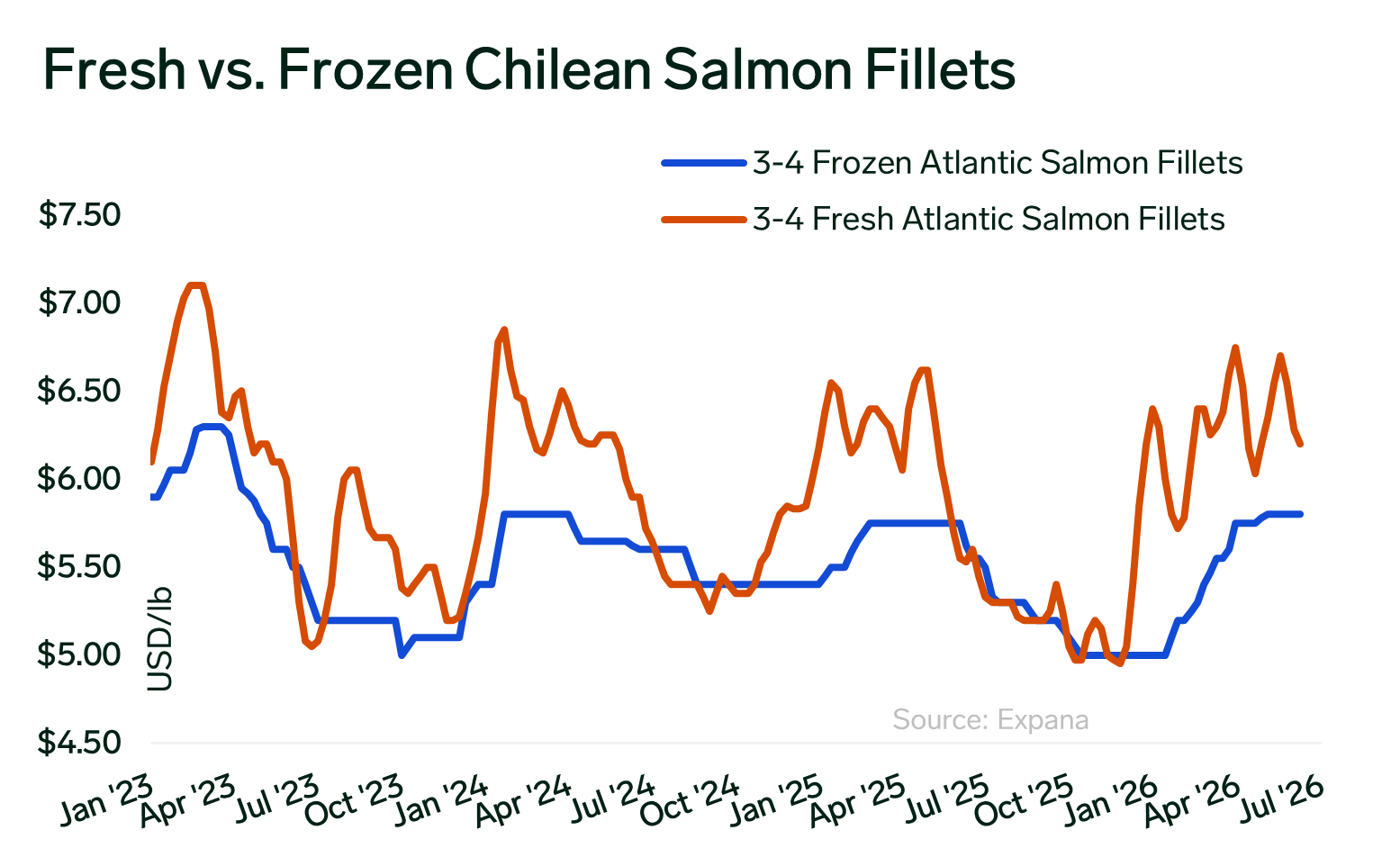

Expana’s June 11 Salmon Market Situation describes the 3-4 lb. fresh benchmark sitting in a $6.20-$6.40/lb range with a barely steady undertone and continued downward pressure. Deal flow is irregular, transactions are occurring both above and below the quotation, and buyer sentiment is cautious. Frozen, by contrast, is rated full steady with some higher offers being collected.

The frozen firmness is not demand-driven. Producers were not freezing material at scale when fresh was soft, leaving domestic frozen stocks lean. New CNF Chile offers are arriving at significantly elevated levels relative to domestic inventory. The frozen line is holding because supply is thin, not because buyers are competing for it.

Where Imports Stand

YTD through April, total fresh fillet arrivals into the US are running at 148.0 million pounds, below the 149.9 million recorded in 2024 and 151.9 million in 2025, though still above 2022’s 143.6 million. The market is softer than the recent run rate, but not at a historically low base.

The frozen picture is more nuanced. YTD frozen arrivals are at 61.6 million pounds, below the three-year average and consistent with the channel’s seasonal pattern, which typically starts lower in the first half and builds through summer and fall. 2026 is tracking that curve but trailing recent norms, which helps explain why domestic frozen inventory is lean and why the frozen price series is holding steadier than the fresh price series.

Within those totals, the origin-level shifts are significant. Norway’s fresh fillet shipments to the US are down 36.4% year-over-year in April and 35.4% year-to-date, a near-exit from the US fresh market. Chilean fresh is up 6.7% in April and 6.0% year-to-date, stepping directly into the gap Norway has vacated. Faroe/Denmark is up 22.8% in April, and Canada is up 71.9%, both growing from smaller bases. The US import market has reorganized around tariff risk, and Chile is currently the primary beneficiary.

The Tariff Complication

All major salmon-supplying nations currently face a 10% US tariff, with Canada the sole exception under USMCA. The proposed Section 301 duty would add a further 12.5% on Chilean and Norwegian product specifically, with written comments due July 6 and a hearing July 7. Faroe/Denmark and Iceland are not on the Section 301 additional duty list, leaving them at the baseline 10% and at a cost advantage relative to Chile and Norway if the proposed duties are implemented.

Canada’s USMCA exemption, which currently puts it at zero tariff, is itself under pressure. As Expana’s Tariff Talks report has noted, USMCA faces expiry risk with no formal Canada-US talks yet underway, making Canada’s tariff position less certain than the current import data would suggest.

On the fresh side, Chilean sellers’ cash-flow preference means they are more likely to absorb part of the tariff hit than to freeze and wait three months for payment. That dynamic keeps fresh supply flowing and limits how much of the cost increase passes through to US buyers, compressing Chilean exporter margins rather than clearing the market higher. On the frozen side, already-lean inventory and below-trend import volumes mean less buffer if new CNF Chile shipments fully price in the tariff.

El Niño, forecast by Expana as potentially the strongest in a century, adds algal-bloom risk to Chilean aquaculture zones, a supply variable that would change the calculus if it materializes through the second half of 2026.

For now, fresh is drifting under quiet demand, and frozen is holding on lean supply. The next move in either direction will likely come from outside the price chart.

For further insight on upcoming El Niño conditions, sign up for our upcoming webinar led by our weather and commodity experts.

FAQs

Why is the fresh salmon price drifting lower despite a significant drop in Norwegian supply?

Chilean producers are keeping fresh shipments moving even in a soft market because fresh transactions settle in around 30 days versus 90+ days for frozen. That cash-flow preference means sellers absorb price pressure rather than redirect product to the freezer, so supply stays elevated and the benchmark drifts down despite the Norwegian shortfall.

Why is the frozen price holding steadier than fresh?

It comes down to supply, not demand. Producers weren’t freezing material at scale when fresh prices softened, leaving domestic frozen stocks lean. With below-trend import volumes adding to that thinness, the frozen line is holding simply because there isn’t much of it — not because buyers are chasing it.

How has the tariff situation reshuffled where US salmon imports come from?

All major suppliers currently face a 10% baseline tariff, with Canada exempt under USMCA. A proposed Section 301 duty would add 12.5% on Chilean and Norwegian product specifically, pushing buyers toward Faroe/Denmark and Iceland, which would stay at the 10% baseline. Canada’s zero-tariff position is also less secure than it looks, with USMCA expiry risk and no formal US-Canada talks underway.

What could shift the market in the second half of 2026?

The main wildcard is El Niño, which Expana forecasts could be the strongest in a century. If it materializes, algal bloom risk in Chilean aquaculture zones could tighten supply meaningfully — changing the calculus for both the fresh and frozen channels heading into a period when frozen imports typically build seasonally.

Written by Janice Schreiber